🤝 Upside Special Report: Sony Acquires STATSports: A Deep-Dive Analysis

On October 8, 2025, Sony announced its acquisition of STATSports, the Northern Ireland–based global leader in wearable GPS tracking and athlete monitoring. The deal marks a major step in Sony’s continued expansion into the sports technology ecosystem — following its earlier investments in Hawk-Eye, KinaTrax, Beyond Sports, and Pulselive.

By adding STATSports to its portfolio, Sony strengthens its control over the data value chain — from collection to visualization — and positions itself as a central player in the race to create unified, multi-source sports intelligence systems.

What We Know About the Deal

Transaction: Sony has acquired a majority stake in STATSports Group. Financial terms were not disclosed.

Company background: Founded in 2008, STATSports supplies wearable tracking systems to elite teams across football, rugby, NFL, and MLB — including Arsenal, Liverpool, Manchester United, Juventus, the England national team, the All Blacks, the LA Dodgers, and multiple NFL franchises.

Official rationale: Sony stated the acquisition would “merge wearable and optical tracking data to deliver the most comprehensive picture of athletic performance.”

Integration: STATSports will maintain its Newry headquarters and R&D operations, integrating its software and data architecture within Sony’s sports tech division.

The Rationale

The acquisition completes a missing piece in Sony’s sports data vision. Optical systems (like Hawk-Eye) capture movement and events, but they lack direct biometric insight. STATSports brings physiological depth — heart rate, acceleration, player load, fatigue — making Sony’s ecosystem more holistic.

This move supports two strategic goals:

Full-stack data integration: Sony can now collect, analyze, and distribute every form of performance data — visual, spatial, and biological.

Market differentiation: Owning the end-to-end data pipeline gives Sony an advantage in offering teams, leagues, and broadcasters a unified product suite instead of fragmented vendor solutions.

How This Complements Sony’s Existing Sports Tech Portfolio

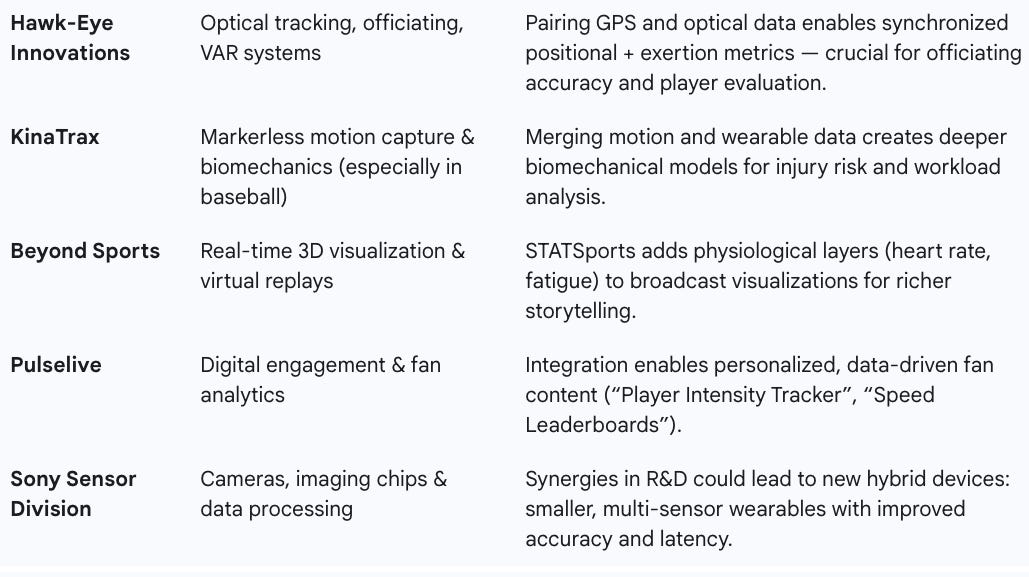

Sony’s acquisition of STATSports fits neatly alongside its growing roster of sports technology subsidiaries and investments:

Source: Upside Global, confidential, October 2025

In short, STATSports fills the biometric and physiological gap in Sony’s stack. It transforms Sony from a collection of data tools into a fully integrated sports performance ecosystem — capable of powering both elite teams and broadcast networks with synchronized, multimodal data.

Why It Makes Sense for Sony and STATSports

For Sony:

Vertical integration: Combines wearable, optical, and visual data in one pipeline.

Expanded monetization: Enables cross-sector offerings — athlete management systems, real-time fan graphics, officiating insights.

Future-proof positioning: Strengthens Sony’s bid to become the backbone of smart stadium and AI-driven performance ecosystems.

For STATSports:

Scale and credibility: Sony’s global reach accelerates growth into new markets.

R&D capacity: Access to Sony’s imaging and sensor technology could yield smaller, smarter, multi-sensor devices.

Cross-platform integration: Synergy with Hawk-Eye and KinaTrax positions STATSports as the physiological engine within Sony’s broader sports architecture.

Impact on the Sports Tech Industry (GPS & Wearables)

Consolidation accelerates. Sony’s acquisition confirms that the future of sports tech lies in platform convergence. Expect more mergers as companies seek to unify capture, analytics, and fan engagement.

Data fusion becomes the new baseline. Teams and leagues will increasingly demand integrated optical + wearable data, pushing vendors to develop interoperability or risk obsolescence.

Pressure on incumbents. Companies like Catapult, Kinexon, and Playermaker must innovate or align strategically to compete with Sony’s end-to-end offering.

Evolving monetization models. Expect new subscription-based analytics layers, predictive insights, and AI-driven dashboards that combine physical and physiological data in real time.

Ethical and ownership challenges. As wearable data becomes a commercial asset, expect heightened debate over athlete privacy, consent, and data rights.

Potential Moves by Competitors

Sony’s move will likely trigger a series of competitive responses across the sports tech landscape:

📡 Catapult Sports (Australia): As the incumbent in GPS wearables, Catapult will likely respond by deepening its integration with third-party video or analytics platforms. Potential acquisitions (e.g., AI video analysis firms) could help Catapult stay relevant against Sony’s end-to-end ecosystem.

⚙️ Kinexon (Germany): Kinexon, known for its real-time localization systems and data fusion capabilities, may position itself as the open platform alternative — emphasizing interoperability with multiple hardware systems. Strategic partnerships with leagues (NBA, Bundesliga) could be expanded to lock in clients.

⚾ Hudl / Wyscout: These video and analytics platforms may accelerate efforts to merge athlete monitoring with performance video, either via acquisitions or data partnerships, particularly in football and collegiate sports.

💡 Amazon Web Services (AWS) and Microsoft Azure Sports: Big tech players could deepen their infrastructure role, providing AI-driven sports analytics pipelines that partner with — or eventually acquire — wearable data providers.

📷 Zebra Technologies & Whoop: Companies focused on biometric and real-time data might pivot toward consumer–pro–hybrid markets, leveraging their brand equity to compete indirectly by focusing on health and recovery ecosystems rather than team-level integration.

📊 Apple and Google (long-term): Both are expected to continue investing in sports health data, especially as wearables (e.g., Apple Watch Ultra, Fitbit) gain credibility in performance environments. Integration with elite sports may soon follow.

In short, Sony’s acquisition will reset competitive expectations — forcing others to choose between specialization (doing one thing exceptionally well) or platform integration (offering an ecosystem). The next 12–18 months could bring a wave of M&A and alliance activity as competitors race to stay relevant.

Conclusion

Sony’s acquisition of STATSports marks a defining moment in the evolution of the sports technology sector. By merging wearables with optical, biomechanical, and visualization tools, Sony now controls a vertically integrated ecosystem that connects performance analysis, officiating, and fan engagement.

For Sony, it’s a platform play. For STATSports, it’s scale and synergy. And for the industry, it’s a signal: the future of sports tech lies not in isolated sensors but in connected ecosystems that turn movement and physiology into actionable intelligence. Competitors will now have to decide — join the ecosystem race or risk being left behind.